PSD2 is the latest, novel European payment regulation that implies access by third parties to banking infrastructure.

The new Payment Services Directive (PSD2) will enter effect in 2018… is your company ready for this change?

What is PSD2?

PSD2 derives from the first Payment Services Directive (PSD), which was enacted in 2007. Its main goal was to create a unique payment market in the Eurozone to boost innovation, competition and efficiency in the European Union.

“With PSD2, the European Union is betting on the development of the online payment market in the Eurozone.”

Years later, in 2013, this directive and its goals were revised. This resulted in PSD2, whose goals are to improve competition among countries and payment providers; innovation in new payment methods – especially online payments via mobile or smartphone –; and, of course, to offer greater protection to the consumer.

Promon.co Blog

What does this new directive imply?

PSD2’s true innovation is opening banking payment services to third parties, known as Third Party Payment Service Providers (TPPs). This means that other companies will have access to customers’ bank accounts – as long as the latter give their express consent –, in addition to being able to make payments on their behalf.

You might be wondering how they will manage to do this… Well, this will be accomplished by means of an API that will facilitate communication between the company and the bank, which will allow the business/establishment to perform payments on behalf of the customer through his bank account.

![]()

WSO2

The inclusion of new players – which is to say, TPPs – implies more competition on the market, since they will try to offer the best and cheapest payment solution to obtain a greater market share.

Eliminating barriers and allowing the arrival of third parties does not imply a greater risk or lower protection, since TPPs will have the obligation to comply with the traditional set of payment standards: registration – authorization – supervision; in addition to increasing safety measures for online payments.

– Discover what WSO2 is and the solutions it provides –

APIs: essential in PSD2

When speaking of PSD2 we must mention APIs. APIs are the cornerstone of the new directive, since they are the technical means that will allow banks to comply with the standards imposed by PSD2.

Despite the fact that many banks have already implemented APIs, some still remain that are yet to do so, and must implement them in their organizations as soon as possible. In light of this, we could say that we are facing a double challenge: complying with the new directive and implementing the APIs, since, as stated by BBVA Spokesman Álvaro Martín, “banks have to control who accesses that information and how it is being used.”

Once APIs have been implemented, they will allow the sharing of information among various providers: PISPs (Payment Initiation Services Providers), which allow customers to make direct payments to a company from their account; and AISPs (Account Information Service Providers), which allow users to get consolidated information on the state of various accounts held at several banks. For example, Fintonic is a fintech that may be considered to be an AISP.

While you might be confused with so many acronyms, what is important is to remember that both PISPs and AISPs are third party payment providers (TPPs).

Thanks to PSD2 – well, more specifically, the APIs –, financial institutions will gain a better knowledge of their customers, which allows them to offer them a personalized product offering, reducing risk.

– You might be interested in this post: Why tailoring your systems to the environment is a MUST –

WSO2 Open Banking

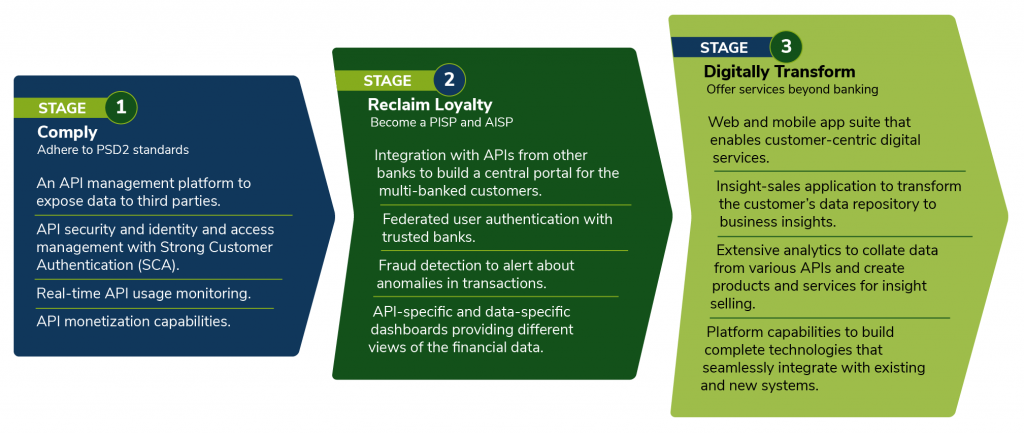

If your company is still not ready for PSD2, you are in luck! Because we want to introduce to you WSO2 Open Banking, the new solution by WSO2 as a response to the new directive.

Ensuring your organization complies with PSD2 is simple, fast and safe with WSO2. It is worth mentioning that, in addition to ensuring compliance with the directive, WSO2 Open Banking will help with the digitalization of your organization, providing support to its priorities.

But what can WSO2 Open Banking do for you? API integration with third parties, PISPs and AISPs; detecting monetization opportunities; integration points with basic banking systems; detecting fraud – in order to do this it offers a powerful, multi-factor, customizable authentication policy as well as consent management –; in addition to default API templates that comply with the Open Banking specifications of major banking organizations.

WSO2 Open Banking

If you want to learn more about the features and benefits of WSO2 Open Banking, as well as the advantages it offers in relation to the new PSD2 directive, do not hesitate to contact us. It will be our pleasure to assist you!